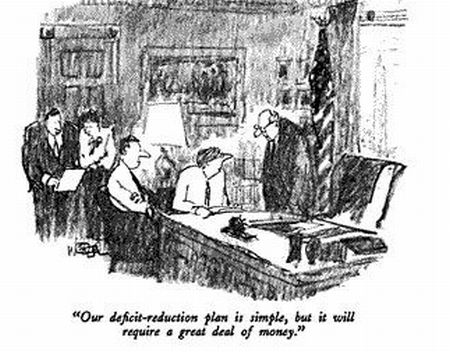

Time to have a little fun with The Capital's editorial staff, who ran an editorial that--much like the title of this post--has urgency only in the fact that it's been going on for a long time. "Our say", they say, is that Washington is going to have to worry about the budget deficit. Alert the press!.....what?? Oh. They've been alerted.

Washington may be hard of hearing, but it is not stone-deaf. If the electorate shouts loudly enough, it reacts. And here's what the voters were saying in this month's election:

Nice [sic] right off the bat with the 'stone-deaf' bit. Good editing, editors. My favorite spelling error is when "it's not" turns into "it snot", a space-bar mistake that I myself rely on Spellcheck to correct. Also I really hope I don't have any errors in this post, because then I would look like a jackass.

Government has gotten too big and can't keep spending money it doesn't have. We've had to cut household expenses back to what we can afford, and we don't see why you politicians can't do so as well. Get this done - or we'll find someone else who can.

This is an editorial comment that was appropriate, like, BEFORE the election. Wtf? In case you didn't realize, most of America did find other people who can reduce the deficit. Or at least say they can. Also, a report from Obviousville confirms that you can't spend money you don't have, at least in the long term, even if you're the government. Also #2, which specific household expenses do you think the editors had to cut? Pipe tobacco? Cognac by the fireplace? Sailboats? What are some other stereotypes?! Actually, that sounds like an awesome lifestyle...does anyone have any VSOP.....

As Sheila C. Bair, the chairwoman of the Federal Deposit Insurance Corp., wrote inThe Washington Post recently, "total federal debt has doubled in the past seven years, to almost $14 trillion. That's more than $100,000 for every American household." Our long-term structural deficit, and the borrowing needed to sustain it, could easily destabilize our finances and wipe out any recovery.

National debt always goes up during war times, but even so, the editors--or 'my homies' as they will be known for the rest of this post--are correct in having concern over ballooning debts. My homies use the term 'structural' deficit to highlight what I just touched upon. War expenditures and economic downturns surely produce cyclical deficits, which are easier to ignore because politicians can proclaim that everyone will resume finding gold bars in their storage sheds once some miscellaneous miracle happens, then they don't have to address the problem. A structural problem implies that even if all the bullshit turns into roses, there would still be a financial imbalance. Also, my guess is that one of my homies bet another one that he/she couldn't reference 'Sheila C. Bair' in a published work, and that bet is now paying off big.

The first remedy Congress has in mind - symbolic but important - is a moratorium on earmarks. This is the practice of slipping funding of individual projects into bills and committee reports, avoiding hearings and circumventing the usual federal budget process.

First of all, does anyone not know what an earmark is? Earmarks are the embodiment of inside-the-beltway politics. Earmarks are why Congress has terrible approval ratings but people's own Congressmen have high ratings. And earmarks are a relatively small portion of the budget. I would be stunned if Congress voted to decrease the advantage of being an incumbent just to save 1% on the federal budget. Plus, I suspect that if specific earmarked projects were ended, some type of direct discretionary funding to states would pop up, which negates the whole point, but is still better (see below).

Earmarking is a treasured perk of the most senior legislators, a way of pleasing constituents (and perhaps rewarding campaign donors). That does not mean that all earmarked projects are bad. But the Tea Party movement has swung the Republican leadership into the anti-earmarking camp, where they are being joined by some Democrats and President Barack Obama.

I tend to agree that not all earmarked projects are bad. I mean, after all, the federal government is a government, and governments are there to spend money on necessary projects that the private market will not facilitate. However, the bigger the particular government that's spending the money, the less likely it's spending money on the right thing. I would much rather the feds give money to the state of Maryland, who then gives the money to Anne Arundel county, who then gives the money to my homeowners association, who then builds a lazy river and pool house in my backyard. See how government can work for you?

Earmarks, however, account for less than 1 percent of federal spending. Two recent reports have sketched out the painful changes that would be needed to really reduce deficits.

Life is full of 'painful changes'. I recently had to downgrade cognacs from VSOP (Very Special Old Pale) to XO (Extra Old), so I know what it's like to make painful changes.

One is by former Clinton White House chief of staff Erskine Bowles and former Republican senator Alan Simpson of Wyoming - the co-chairmen of a presidential deficit reduction commission that is supposed to report its findings on Wednesday. The other is by the independent Bipartisan Policy Center. Both documents have been under withering attack - by conservatives because they recommend raising some taxes, by liberals because they seek cutbacks in Medicare and Social Security.

Fat chance that I'm going to look up these reports, so let's just ignore that paragraph. However, if any proposal is hated by both sides of the political aisle, it's probably a good proposal.

Before joining such denunciations, people need to grasp the facts laid out in the Bipartisan Policy Center report: Medicare and Medicaid consume 21 percent of federal spending. Social Security accounts for another 20 percent. Defense requires 20 percent. Other mandated spending (on such things as veterans' compensation, unemployment insurance and food stamps) takes up 17 percent. Paying the interest on the national debt requires 6 percent.

Translation:

-necessary evils, defense, government waste, and bullcrap mandated by law account for 84% of the budget.

So everything else is just 16 percent of the budget. The budget can't possibly be balanced just from that 16 percent.

It's even worse for the city of Annapolis, where 85% of the budget is salaries and wages, 10% is corruption, 7% is illegal payments to bloggers, and -2% is money regained by stealing the lunch money from St. Mary's students and midshipmen.

Also, without knowing the numbers off the top of my head, I initially doubted the claim that the federal budget 'can't possibly be balanced' by a 16% adjustment'. Then I looked it up. OMG. The federal budget deficit for 2010 is 49%. The government proposed spending 49% more money (like $1.2 trillion more) than they plan on taking in. Take a second to absorb that, then take a minute to pour yourself a cocktail, because XO cognac is the only thing that will make spending $1,200,000,000,000 that you don't have seem like an acceptable thing to do.

Deficit reduction will be the big domestic political challenge of 2011, and possibly for years after that. It urgently needs presidential leadership. And it will require our two polarized political parties to come together and strike a compromise in the national interest.

If that seems like too much for today's pols, they should remember the message of the election. If they can't do it, the voters will find people who can.

Entitlement programs and mandated spending must be overhauled. Hopefully the voters can provide the accountability to make this happen. It's not just the political challenge of 2011; it's a challenge for many political and socio-economic cycles to come.

Sunday, November 28, 2010

Thursday, November 25, 2010

Thursday, November 18, 2010

Incentives Are the Difference Between Public and Private Sector Workers

It was probably a year ago that I cancelled my subscription to The Capital--not in protest or anything because I do enjoy reading it, but for 2 reasons. First, I found that on most days I would just recycle it without reading anything, and second because I found a more efficient way to line my outdoor table for eating crabs. I kept my paper box, however, because I still wanted to receive the lovely landscaping flyers and community propaganda and that type of stuff can't go in the mailbox!

Consequently, it's more difficult to use letters to the editor as blog fodder. The best source of opinion now is probably the commenters on the Capital's web site, a crowd of probably 30 regulars that sling entrenched opinions from the comfort of computer screens. Little known fact: every year the online opinion world competes in the "Mom's Basement Bowl", whereby competitors try and type the nastiest slur possible while eating a bowl of chips and dip. Last year I came in 5th place. (My dip was too thick and my chip broke in half just as I was about to lay into the Deputy Streetsweeper. Major disappointment.)

So I was looking through the comments on this story, and a mini debate erupted regarding workers in the private sector vs. the government sector. The current paradigm of course is that private sector workers think that government workers meet for happy hour every day at 2 pm on a beach in the Bahamas, and government workers think that private sector workers ignore the vital role of government employees, which the private sector workers are too greedy and selfish to ever do themselves. As always the truth is somewhere in the middle.

There are lazy people and hard working people in both sectors. The Annapolis City Clerk, for example, is one of the best government employees I've ever come across. The base city clerk salary I think might be $70-$75k, with benefits pushing the total compensation to $90k ish off the top of my head. Fair cost to taxpayers? Could someone willing to work for $20k less do the same job? Does a private sector worker making $50k require the same job skills? Hard to say.

The problem is incentives. Private sector employees have an incentive to work hard because if not they will get fired. Businesses pay their employees with their money--it's an investment. If the investment doesn't pay off, the employee doesn't work there anymore. I can't really think of an example of tenure in the private sector. Maybe unions offer some type of protection for seniority, maybe other examples exist that I don't know about. But governments are a different story. The people that pay the salaries of government workers (you) don't have a say in how these workers do their jobs. That's the problem. Government managers don't have as profound an incentive to keep their workers productive because they are paying them with a third party's money.

My guess is that workers that coast through their jobs (in either sector) are workers that have no mobility, either upward or downward. Or 'outward' I guess--gotta get all the 'ward's in there. With no fear of being fired, and no possibility for advancement, why work hard? Maybe an intrinsic work ethic keeps you busting your butt for a while, but eventually you realize you get the same money no matter how much work you do.

I do think the government has been trying to place more incentives for pay raises based on merit. I think this only on the basis of knowing that my brother, who works for the IRS, makes more money if he does more stuff like get continuing education or whatever. Even so, a recent study found that all things considered the average federal worker makes double what the average private sector worker makes. Theoretically a cost of living raise should match inflation, but the raises received by government workers have outpaced inflation by 33% since 2000.

Some job requirements of government workers wouldn't be tolerated by the private sector. The city clerk, for example, has to work from 7 pm to 11 pm every other Monday night, and sometimes has to stay at the office until midnight in case candidates want to file for election at the 11th hour. How much overtime would have to be paid to a private sector employee to do the same?

I am confident that good and bad employees exist in both sectors. I am also confident that government is less efficient than the private sector--much of my political belief system relies on this confidence. The government will never be able to provide the same incentives that markets do, which I believe is why we should have as little government as possible.

Consequently, it's more difficult to use letters to the editor as blog fodder. The best source of opinion now is probably the commenters on the Capital's web site, a crowd of probably 30 regulars that sling entrenched opinions from the comfort of computer screens. Little known fact: every year the online opinion world competes in the "Mom's Basement Bowl", whereby competitors try and type the nastiest slur possible while eating a bowl of chips and dip. Last year I came in 5th place. (My dip was too thick and my chip broke in half just as I was about to lay into the Deputy Streetsweeper. Major disappointment.)

So I was looking through the comments on this story, and a mini debate erupted regarding workers in the private sector vs. the government sector. The current paradigm of course is that private sector workers think that government workers meet for happy hour every day at 2 pm on a beach in the Bahamas, and government workers think that private sector workers ignore the vital role of government employees, which the private sector workers are too greedy and selfish to ever do themselves. As always the truth is somewhere in the middle.

There are lazy people and hard working people in both sectors. The Annapolis City Clerk, for example, is one of the best government employees I've ever come across. The base city clerk salary I think might be $70-$75k, with benefits pushing the total compensation to $90k ish off the top of my head. Fair cost to taxpayers? Could someone willing to work for $20k less do the same job? Does a private sector worker making $50k require the same job skills? Hard to say.

The problem is incentives. Private sector employees have an incentive to work hard because if not they will get fired. Businesses pay their employees with their money--it's an investment. If the investment doesn't pay off, the employee doesn't work there anymore. I can't really think of an example of tenure in the private sector. Maybe unions offer some type of protection for seniority, maybe other examples exist that I don't know about. But governments are a different story. The people that pay the salaries of government workers (you) don't have a say in how these workers do their jobs. That's the problem. Government managers don't have as profound an incentive to keep their workers productive because they are paying them with a third party's money.

My guess is that workers that coast through their jobs (in either sector) are workers that have no mobility, either upward or downward. Or 'outward' I guess--gotta get all the 'ward's in there. With no fear of being fired, and no possibility for advancement, why work hard? Maybe an intrinsic work ethic keeps you busting your butt for a while, but eventually you realize you get the same money no matter how much work you do.

I do think the government has been trying to place more incentives for pay raises based on merit. I think this only on the basis of knowing that my brother, who works for the IRS, makes more money if he does more stuff like get continuing education or whatever. Even so, a recent study found that all things considered the average federal worker makes double what the average private sector worker makes. Theoretically a cost of living raise should match inflation, but the raises received by government workers have outpaced inflation by 33% since 2000.

Some job requirements of government workers wouldn't be tolerated by the private sector. The city clerk, for example, has to work from 7 pm to 11 pm every other Monday night, and sometimes has to stay at the office until midnight in case candidates want to file for election at the 11th hour. How much overtime would have to be paid to a private sector employee to do the same?

I am confident that good and bad employees exist in both sectors. I am also confident that government is less efficient than the private sector--much of my political belief system relies on this confidence. The government will never be able to provide the same incentives that markets do, which I believe is why we should have as little government as possible.

Tuesday, November 16, 2010

Brothel Raided

A brothel?! Geez.

This particular operation involved illegal immigrants, but whether we talking about illegal citizens or just criminal citizens that are here legally, I take it as a sign of importance that zoning laws are enforced.

It's kind of like how there's no such thing as a routine traffic stop. All the stuff about the number of unrelated people living in a house, number of cars in the driveway, etc. can help law enforcement snuff out bigger stuff like this.

This particular operation involved illegal immigrants, but whether we talking about illegal citizens or just criminal citizens that are here legally, I take it as a sign of importance that zoning laws are enforced.

It's kind of like how there's no such thing as a routine traffic stop. All the stuff about the number of unrelated people living in a house, number of cars in the driveway, etc. can help law enforcement snuff out bigger stuff like this.

Monday, November 15, 2010

Pensions: You Mean Paying Someone to do Nothing Doesn't Work?

The Capital highlights a problem that has been creeping up since, well, since pensions began. (See HERE and HERE). Labor economics theory predicts that a person will be paid an amount roughly equal to the value of what they produce. The key here is that a person has to be producing something of value, i.e. working, in order to earn a salary.

Unlike 401K's, which are investments that provide a variable rate of return, pensions are guaranteed future payments.

Problem #1: Pension funds rely on markets to grow their asset base and meet their obligations, and markets are variable.

Problem #2: The longer somebody works for a company / the government, the bigger the pension. So, the more well trained the workforce, the more of an advantage a company has, but it also has a higher future labor cost, so it has a relative disadvantage. See the paradox?

Problem #3: The burden of funding pensions falls disproportionately on the employer as compared to other fringe benefits.

Problem #4: Taxpayers are on the hook for existing pension obligations--they cannot be adjusted ex post facto.

The main problem is #1. Pensions assume a certain rate of return that probably won't happen. 5 years ago, AACo's pension was like 98% funded. Now it's 85% funded according to one of those articles up there. This is because the rate of return on their assets was not what they expected, and they couldn't divert enough of our tax money to make up the difference.

Pensions have already destroyed the competitiveness of American automakers, who might very well shift their pension liabilities to you and me. Governments aren't competitive in anything, so their pension cost goes directly to us.

Fringe and retirement benefits need to be able to move up and down (specifically down) with market movements. Pensions do not allow for this. More appropriate benefits would be 401K's or other investment accounts. Hopefully the transition can be made soon enough.

Sunday, November 14, 2010

What Makes A Successful Entrepreneur

1. Be Passionate and Have a 99% Commitment.

The most important thing in starting a successful business is not having a good idea or product. It's not even having a good team or being well capitalized. It's having passion; it's having the vision and determination to know that even though other people could do what you do, your way of doing things is going to change the world. This passion should manifest itself into a 99% commitment to your business. Anyone who tells you that you should be 100% committed hasn't really thought it through and is just bullshitting you. Your dear mother, who raised you and is the reason for everything you are today, has fallen ill and is in the hospital. You cut out of work early to go visit her--THAT'S the 1%. To start a business, the rest of the 99% of you has to be committed to the business, and you must be willing to make sacrifices.

My experience: I started my business 2 weeks after my 21st birthday, and a year before receiving a good degree in a relatively good job market. While my friends were moving up the corporate ladder during the day and exploring the 'youth + money = fun life' equation, I was working. I slept at the office as much as at my house, and picked up odd jobs to pay the bills. The pinnacle came in one month of 2005, as I remember, when I worked 120 hours in each week of the month. I slept every other night and ignored every other aspect of my life. Is this how it should be forever...of course not. But it's what was needed at the time.

2. Have a Hatred of Failure--Not a Fear of It.

There's no denying that being a successful entrepreneur requires a certain disposition towards risk. On occasion, this is going to mean you fail. No single bet should be so great that could potentially bankrupt the company. If things you try fail, you can't let it dissuade you. You have to learn from your screw up, double down, and vow that the same mistake will never happen again. If you're failure results in the company going under, use it as a chip on your shoulder to start the next one.

My experience: In addition to my main company, I've had 2 unsuccessful spin-offs during the 8 years in business. I had a deli in 2005 that basically broke even for a year, but prospects were declining, and I was tired of working for free at a job with miserable hours. More painfully, I was a co-owner of a college bar where I operated the kitchen for about 14 months. Initial projections were wrong, and despite 4 menu changes and continuous improvements over that time, I lost like $65,000. Boo. As I write this, a year and a half after it's over, it still makes me sick. But that's the correct feeling. My experiences gained are invaluable, and I try and use them as motivation to keep on pushing forward.

3. Don't Lose Track of the Money.

This seems obvious, but it can be difficult. This advice is particularly important for young entrepreneurs, but anyone owning a business for the first time or recognizing a life-long dream can fall victim. Owning a business can be thrilling. You have total creative power to bring your vision to fruition, and sometimes the passion (remember from #1 that passion is involved) causes business owners to turn a blind eye to the money. Sometimes you are so exited to serve that new recipe; to get home at night completely exhausted from a day's work; to romanticize the experience, that you ignore the common sense analyses that are needed to make sure you'll be able to pay the bills. Every decision made must be the best effort to maximize the long term profitability of the business. Now does this mean that the cheapest option is always preferred? No! Certain investments yield long term results. However, profits need to be realized somewhat quickly. If cash flow is achieved through slim margins or debt, the long term health of the business could be in jeopardy.

My experience: I lost track big time. As mentioned, I was a young know-nothing when the company started. After I graduated from college (year 1 of the business), the company grew by 500%. I didn't know what to do, so I did what I thought I should do--what 'real companies' do. I hired too many managers and took out a lease on a office that did nothing to increase revenues or profits. By the time I realized this, I was $75k into debt with a business model that shouldn't have needed more than $10k in capital. Total jackass maneuver on my part. Moreover, I was paranoid that customers wouldn't trust a 21 year old kid to deliver on promises, so I gained business by underpricing our services. Even though I now increase prices each year, our old customers are far less profitable than the new customers, and they will probably never catch up. Eight years ago, I essentially sold out to 'buy' cash flow, and today the effects are still being felt.

4. Dream Big.

Especially for companies in early stages, it's quite easy for owners to get caught up in the day-to-day and ignore the long-term. This is not good. 'Appropriate egomania' is the oxymoron that I would use to describe the requirement that you believe that you can do things better than anyone else, and that the possibilities for your business don't stop at what you can see in the near future, but rather are infinite. Take the time to think about a 5 year plan, and make sure that every thing you do in the short term fits in to where you want to take the company in the long term.

My experience: It took me a long time to learn this lesson. Like many entrepreneurs, I was heavily involved in operations in the beginning because I couldn't afford to pay someone else to handle the day-to-day operations while I focused on strategy. My 'holy shit' moment came from a business competition, sponsored by the founder of Under Armour, that gave $15,000 to the winner and $7,500 to 2nd place. I delivered a great presentation, highlighting all the logistics and details that I thought made us the best. After the judges deliberated, they started with their presentation...."Before we announce the first and second place winners"--they turned to me--I knew right away I hadn't won. "Brian, we think you can grow faster than you think you can. Scalability, reproducing what you do now over and over again: that's the future, that's the business model". I was devastated, but the judges rightfully recognized that I wasn't dreaming big. While the other businesses offered figures for what their total potential market was--numbers in the hundreds of millions of dollars that would probably never be realized--I mentioned only what I charged the current customers. If you don't think you can be big, then you can't. So think it.

5. Luck.

Shit happens. And at least some of the shit needs to happen in your favor for you to be successful.

My experience: I started my company because I knew how to cook and I was in a fraternity. I was in a fraternity because a friend bugged me to go to a rush event and some guy bought me a piece of pizza. I was at the University of Maryland because I had met a professor at the yacht club I used to work at, and because I was denied admission to the University of Pennsylvania (assholes). I knew how to cook because my paper route wasn't keeping up with the rising cost of Air Jordans in 1997, and I figured a restaurant was better than folding sweaters at the Gap. If any of those things hadn't happened, I probably wouldn't own a business today. The goal is to be well prepared to when fortune falls in your favor, you can capitalize on it.

Want to know more:

Characteristics of Successful Entrepreneurs, from Maryland's 'Godfather of Entrepreneurship'

Book: Good to Great

Book: Built to Last

The most important thing in starting a successful business is not having a good idea or product. It's not even having a good team or being well capitalized. It's having passion; it's having the vision and determination to know that even though other people could do what you do, your way of doing things is going to change the world. This passion should manifest itself into a 99% commitment to your business. Anyone who tells you that you should be 100% committed hasn't really thought it through and is just bullshitting you. Your dear mother, who raised you and is the reason for everything you are today, has fallen ill and is in the hospital. You cut out of work early to go visit her--THAT'S the 1%. To start a business, the rest of the 99% of you has to be committed to the business, and you must be willing to make sacrifices.

My experience: I started my business 2 weeks after my 21st birthday, and a year before receiving a good degree in a relatively good job market. While my friends were moving up the corporate ladder during the day and exploring the 'youth + money = fun life' equation, I was working. I slept at the office as much as at my house, and picked up odd jobs to pay the bills. The pinnacle came in one month of 2005, as I remember, when I worked 120 hours in each week of the month. I slept every other night and ignored every other aspect of my life. Is this how it should be forever...of course not. But it's what was needed at the time.

2. Have a Hatred of Failure--Not a Fear of It.

There's no denying that being a successful entrepreneur requires a certain disposition towards risk. On occasion, this is going to mean you fail. No single bet should be so great that could potentially bankrupt the company. If things you try fail, you can't let it dissuade you. You have to learn from your screw up, double down, and vow that the same mistake will never happen again. If you're failure results in the company going under, use it as a chip on your shoulder to start the next one.

My experience: In addition to my main company, I've had 2 unsuccessful spin-offs during the 8 years in business. I had a deli in 2005 that basically broke even for a year, but prospects were declining, and I was tired of working for free at a job with miserable hours. More painfully, I was a co-owner of a college bar where I operated the kitchen for about 14 months. Initial projections were wrong, and despite 4 menu changes and continuous improvements over that time, I lost like $65,000. Boo. As I write this, a year and a half after it's over, it still makes me sick. But that's the correct feeling. My experiences gained are invaluable, and I try and use them as motivation to keep on pushing forward.

3. Don't Lose Track of the Money.

This seems obvious, but it can be difficult. This advice is particularly important for young entrepreneurs, but anyone owning a business for the first time or recognizing a life-long dream can fall victim. Owning a business can be thrilling. You have total creative power to bring your vision to fruition, and sometimes the passion (remember from #1 that passion is involved) causes business owners to turn a blind eye to the money. Sometimes you are so exited to serve that new recipe; to get home at night completely exhausted from a day's work; to romanticize the experience, that you ignore the common sense analyses that are needed to make sure you'll be able to pay the bills. Every decision made must be the best effort to maximize the long term profitability of the business. Now does this mean that the cheapest option is always preferred? No! Certain investments yield long term results. However, profits need to be realized somewhat quickly. If cash flow is achieved through slim margins or debt, the long term health of the business could be in jeopardy.

My experience: I lost track big time. As mentioned, I was a young know-nothing when the company started. After I graduated from college (year 1 of the business), the company grew by 500%. I didn't know what to do, so I did what I thought I should do--what 'real companies' do. I hired too many managers and took out a lease on a office that did nothing to increase revenues or profits. By the time I realized this, I was $75k into debt with a business model that shouldn't have needed more than $10k in capital. Total jackass maneuver on my part. Moreover, I was paranoid that customers wouldn't trust a 21 year old kid to deliver on promises, so I gained business by underpricing our services. Even though I now increase prices each year, our old customers are far less profitable than the new customers, and they will probably never catch up. Eight years ago, I essentially sold out to 'buy' cash flow, and today the effects are still being felt.

4. Dream Big.

Especially for companies in early stages, it's quite easy for owners to get caught up in the day-to-day and ignore the long-term. This is not good. 'Appropriate egomania' is the oxymoron that I would use to describe the requirement that you believe that you can do things better than anyone else, and that the possibilities for your business don't stop at what you can see in the near future, but rather are infinite. Take the time to think about a 5 year plan, and make sure that every thing you do in the short term fits in to where you want to take the company in the long term.

My experience: It took me a long time to learn this lesson. Like many entrepreneurs, I was heavily involved in operations in the beginning because I couldn't afford to pay someone else to handle the day-to-day operations while I focused on strategy. My 'holy shit' moment came from a business competition, sponsored by the founder of Under Armour, that gave $15,000 to the winner and $7,500 to 2nd place. I delivered a great presentation, highlighting all the logistics and details that I thought made us the best. After the judges deliberated, they started with their presentation...."Before we announce the first and second place winners"--they turned to me--I knew right away I hadn't won. "Brian, we think you can grow faster than you think you can. Scalability, reproducing what you do now over and over again: that's the future, that's the business model". I was devastated, but the judges rightfully recognized that I wasn't dreaming big. While the other businesses offered figures for what their total potential market was--numbers in the hundreds of millions of dollars that would probably never be realized--I mentioned only what I charged the current customers. If you don't think you can be big, then you can't. So think it.

5. Luck.

Shit happens. And at least some of the shit needs to happen in your favor for you to be successful.

My experience: I started my company because I knew how to cook and I was in a fraternity. I was in a fraternity because a friend bugged me to go to a rush event and some guy bought me a piece of pizza. I was at the University of Maryland because I had met a professor at the yacht club I used to work at, and because I was denied admission to the University of Pennsylvania (assholes). I knew how to cook because my paper route wasn't keeping up with the rising cost of Air Jordans in 1997, and I figured a restaurant was better than folding sweaters at the Gap. If any of those things hadn't happened, I probably wouldn't own a business today. The goal is to be well prepared to when fortune falls in your favor, you can capitalize on it.

Want to know more:

Characteristics of Successful Entrepreneurs, from Maryland's 'Godfather of Entrepreneurship'

Book: Good to Great

Book: Built to Last

Wednesday, November 10, 2010

Lower Corporate Taxes Mean More Jobs, Which Means More Tax Revenue

Let's get something out of the way first. I love corporations. I think they're great. The public tends to support the abstract of small businesses over that of big businesses, even though every big business was at one time a small business. Moreover, I don't hate on corporations for making big profits, even obscene profits. If a company does such an expert job at whatever they do to earn a profit of a billion dollars in a quarter, more power to them. As long as the market is free of coercion, profits represent mutually agreed upon transactions that make both the buyer and the seller better off than they were before. If a company makes $1 billion, it means that people like me and you are $1 billion better off than we were before. Do you and I want to figure out how to build our own cars?...to mine the aluminum, shape the rubber for the tires? Do you and I want to drill for oil in deep ass water in the middle of hurricanes? No...you and I can't even make it to the bank before it closes. We need corporations so we can pay them to do what they do best, and sell them the things we do better than them.

Partially because people don't like corporations, but mostly because states want more money, there is always talk about closing tax loopholes and collecting more money from corporations. I'm all about abiding by the law, but there's some things to think about.

If taxes are high, businesses will try to avoid them. For our purposes we'll talk about the legal ways. For companies doing business in multiple states, they'll concentrate operations in the states that give them the lowest tax burden. They will hire workers in those states, and those workers will create income, property, and payroll taxes. States with high taxes will chase businesses out and actually lose tax revenue, even though they tried to raise the tax rate, a concept credited to an economist named Arthur Laffer.

Businesses want low taxes, but almost as important is consistency. If a certain tax, fee, permit, or bureaucratic red tape exists, even if it's terrible, businesses can figure out a way to deal with it if they have certainty for the future. Just so you don't think I'm making this crap up, I've found some examples of this whole concept at work for your reading pleasure.

When Daimler merged with Chrysler, they headquartered in Germany to enjoy an effective tax rate 23% lower.

Google, Facebook, and others use legal multi-national businesses to pay a 2% effective tax rate.

Iceland slashes corporate tax rate and enjoys higher tax revenue.

Partially because people don't like corporations, but mostly because states want more money, there is always talk about closing tax loopholes and collecting more money from corporations. I'm all about abiding by the law, but there's some things to think about.

If taxes are high, businesses will try to avoid them. For our purposes we'll talk about the legal ways. For companies doing business in multiple states, they'll concentrate operations in the states that give them the lowest tax burden. They will hire workers in those states, and those workers will create income, property, and payroll taxes. States with high taxes will chase businesses out and actually lose tax revenue, even though they tried to raise the tax rate, a concept credited to an economist named Arthur Laffer.

Businesses want low taxes, but almost as important is consistency. If a certain tax, fee, permit, or bureaucratic red tape exists, even if it's terrible, businesses can figure out a way to deal with it if they have certainty for the future. Just so you don't think I'm making this crap up, I've found some examples of this whole concept at work for your reading pleasure.

When Daimler merged with Chrysler, they headquartered in Germany to enjoy an effective tax rate 23% lower.

Google, Facebook, and others use legal multi-national businesses to pay a 2% effective tax rate.

Iceland slashes corporate tax rate and enjoys higher tax revenue.

Sunday, November 7, 2010

Former Annapolis Mayor Commits Suicide (30 years ago) Due to Budget, and Other Observations

Really? Geez. That tragic piece of history, previously unknown to me due to age and other detriments, at least offers the refreshing bittersweet quality that an elected official would actually care that much about taxpayer money.

A friend of mine's father was in charge of preparing a county budget, and as a kid I always chuckled when he worked late during "budget time", because I wondered what was going on during the majority of the months during the year when it was not budget time. The truth is, there's a reason why municipal budget officers routinely garner some of the highest salaries in government. Government finance is complex, plus you're spending other people's money, and those people often get pissed about how you are spending it.

Josh Stewart took a look at historical budgets and provided his insights in the paper today. Josh, I imagine, finds himself in a place I've found myself many times before. It's a lonely place, where untold hours of digging through boring documents yields results only marginally different from what other, lazier people who didn't look anything up will claim to have known all along.

So, here's some stuff that stuck out to me.

This isn't an "in my day a Coke cost a nickel" situation. Theoretically inflation adjusted (a.k.a. "real") figures would stay roughly the same as long as the level of services stayed roughly the same. In 2000, when the real per capita tax was $257, we had police and firefighters. In 2010 we have police and firefighters, but real per capita tax is 53% higher. I can't emphasize enough the difference between 'real' and 'nominal' figures. A 53% increase over 10 years in nominal terms is equivalent to, say, a glass of wine with dinner. A 53% increase over 10 years in real terms is like chugging heroin out of a fire hose. So what's the main difference in the political landscape that occurred between 2000 and 2010? That's right: blogging! We require annual bribes to avoid publishing detrimental things about politicians we know are doing a bad job. Your tax money paid for the heroin hose I am using while writing this post right now! Just kidding.

Governments have only a loose incentive to be responsible with money. The stronger and more direct incentive is for them spend money in a way that helps their short term political career. Time shall ever bear witness to how the city deals with this problem.

A friend of mine's father was in charge of preparing a county budget, and as a kid I always chuckled when he worked late during "budget time", because I wondered what was going on during the majority of the months during the year when it was not budget time. The truth is, there's a reason why municipal budget officers routinely garner some of the highest salaries in government. Government finance is complex, plus you're spending other people's money, and those people often get pissed about how you are spending it.

Josh Stewart took a look at historical budgets and provided his insights in the paper today. Josh, I imagine, finds himself in a place I've found myself many times before. It's a lonely place, where untold hours of digging through boring documents yields results only marginally different from what other, lazier people who didn't look anything up will claim to have known all along.

So, here's some stuff that stuck out to me.

Consider these inflation-adjusted figures: In 1990, the average Annapolitan paid $302 in taxes. Ten years later (in 2000), it was $257. Today, it's $394.(Man, they must have a used a really early base year to calculate those inflation adjusted figures. In 2010 dollars people are paying like $5k-$10k ish and up just in property taxes. If you don't care about base years, just ignore this writing. It's inside parentheses; it's ok. Shout out to my statistician homies who care about this nonsense.)

This isn't an "in my day a Coke cost a nickel" situation. Theoretically inflation adjusted (a.k.a. "real") figures would stay roughly the same as long as the level of services stayed roughly the same. In 2000, when the real per capita tax was $257, we had police and firefighters. In 2010 we have police and firefighters, but real per capita tax is 53% higher. I can't emphasize enough the difference between 'real' and 'nominal' figures. A 53% increase over 10 years in nominal terms is equivalent to, say, a glass of wine with dinner. A 53% increase over 10 years in real terms is like chugging heroin out of a fire hose. So what's the main difference in the political landscape that occurred between 2000 and 2010? That's right: blogging! We require annual bribes to avoid publishing detrimental things about politicians we know are doing a bad job. Your tax money paid for the heroin hose I am using while writing this post right now! Just kidding.

Moyer stands by her fiscal policy and has a stack of reports that give a glowing view of her eight years in office. Yes, her budgets grew, she said, but only because she chased millions in federal grants and tackled long-planned construction projects.So, for 8 of the years responsible for the 53% real tax increase, Moyer was mayor. If her claims that she "chased" more money are true, then the real tax rate wouldn't have had to increase to fund the budgets. Plus, if anything I would guess that Mayor Cohen is more likely to chase money, as he still finds favor with the state party peeps that hand out those grants and governmental transfers. Is there any reason not to assume he'd be able to get the same amount of federal grants? (Answer: no)

Governments have only a loose incentive to be responsible with money. The stronger and more direct incentive is for them spend money in a way that helps their short term political career. Time shall ever bear witness to how the city deals with this problem.

Saturday, November 6, 2010

Mindless Blogging

When I saw a letter to the editor entitled "Republicans Offer Mindless Opposition", I knew I had to spring into action. Everyone knows that Republicans offer mindless support; get with it. Anyway, time to bring back my favorite type of post: the unilateral debate*. Here's how this works. I will post the original text from the letter in a different font, then go point-counterpoint with the letter writer, gradually propping up or shooting down all of his/her arguments. The beauty of this is that the person cannot defend themselves, and consequently all of my points are made eloquently and convincingly, allowing me to persuade everyone as to the accuracy of my insights.

(*"unilateral debate" is the worst name ever, and I literally stopped writing this post for a minute to try and come up with a better name. But then my coffee became ready, and I stopped caring. If you have a better name for this I'll be happy to include it.)

In deciding how to vote. I hope that your undecided readers will carefully weigh what the Democrats and Republicans have done for the American people the past four years.

How people decide who they are voting for always fascinates me. The mysterious "undecided voter" is ever the subject of political rhetoric. And rhetoric, as defined by my high school government teacher is "the philosophy of talk....bullshit....I don't know". The more I learn about political rhetoric, the more correct I realize Mr. Kirby was.

Here's an homage to undecided voters.

Let's continue. Charles from Gambrills is about to drop a Democrat talking point bomb on us. Let's diffuse them one at a time.

The record is clear. In the face of mindless Republican opposition, the Democrats have pulled us back from the brink of depression,

A recession is defined as 2 consecutive quarters of contracting GDP. A depression is a little more abstract, assumed to be 2 years of recession in a row or downturns that have such a level of severity that they cannot be explained by business cycles. So, are we in a depression? No. But did the Democrats save us from it? No. However, the bigger problem is that government economic policy is most likely to affect short term results at the expense of long term growth.

made sure that millions will soon have access to medical care,

which is going to reduce employment, increase premiums, increase taxes, and reduce long term economic prosperity.

made education affordable for millions of students and put us on the road to recovery.

I think the education thing is meant to distract us so I'm just going to ignore it.

If the Republicans win, they intend to sweep away these reforms for the American people and go back to the failed Bush/Cheney policies that ran us into the ditch. We have seen the Republicans in action the party of no has done everything in their power to obstruct the progress our country so desperately needs. The Republicans even oppose President Obama's long term plan to balance the budget while providing a short term stimulus to repair our dangerously deteriorated bridges, dams and airports.

Republicans intend to sweep away Obama/Pelosi/Reid reforms: true.

How people decide who they are voting for always fascinates me. The mysterious "undecided voter" is ever the subject of political rhetoric. And rhetoric, as defined by my high school government teacher is "the philosophy of talk....bullshit....I don't know". The more I learn about political rhetoric, the more correct I realize Mr. Kirby was.

Here's an homage to undecided voters.

Let's continue. Charles from Gambrills is about to drop a Democrat talking point bomb on us. Let's diffuse them one at a time.

The record is clear. In the face of mindless Republican opposition, the Democrats have pulled us back from the brink of depression,

A recession is defined as 2 consecutive quarters of contracting GDP. A depression is a little more abstract, assumed to be 2 years of recession in a row or downturns that have such a level of severity that they cannot be explained by business cycles. So, are we in a depression? No. But did the Democrats save us from it? No. However, the bigger problem is that government economic policy is most likely to affect short term results at the expense of long term growth.

made sure that millions will soon have access to medical care,

which is going to reduce employment, increase premiums, increase taxes, and reduce long term economic prosperity.

made education affordable for millions of students and put us on the road to recovery.

I think the education thing is meant to distract us so I'm just going to ignore it.

If the Republicans win, they intend to sweep away these reforms for the American people and go back to the failed Bush/Cheney policies that ran us into the ditch. We have seen the Republicans in action the party of no has done everything in their power to obstruct the progress our country so desperately needs. The Republicans even oppose President Obama's long term plan to balance the budget while providing a short term stimulus to repair our dangerously deteriorated bridges, dams and airports.

Republicans intend to sweep away Obama/Pelosi/Reid reforms: true.

Failed Busch/Cheney policies ran us into the ditch: false*.

My car is in the shop because I ran it into the Busch/Cheney ditch: false (a runaway tire hit it on the beltway).

Republicans are the party of no: false.

Obama has a long term plan to balance the budget: comical. Also, it's easy to balance the budget if you raise taxes--that's the whole problem.

*The recession was caused mostly by loose credit and a housing price bubble, particularly as a result of Fannie and Freddie. R's and D's I'm sure share the blame for lack of oversight, but it was Democrat Barney Frank who had the most power to affect the policies that led to the recession, but denied the existence of a problem even as the recession had started:

The Republicans have no credible plan to recover from recession. The Democrats are better able to balance the budget, witness President Clinton's large surplus and President George Bush's massive deficit at the end of their terms.

I don't know if Clinton had a surplus at the end of his term, and I'm not going to find out because I've already looked up a lot of shit for this post. So, if he did have a surplus, it's because of a positive business cycle, capital gains and income taxes from an asset bubble, and lack of a major war. Plus, using the deficits at the end of 2 particular Presidents' terms to prove that Democrats better balance the budget is the worst way to prove something since O.J. Simpson's glove.

Also, the credible way to recover from recession is to let producers keep more more of their own money so they can hire more people and invest in future production.

If the Republicans win the next election, they intend to go back to the disastrous policies of President Hoover that led to the great depression. Having run the economy into the ditch, they now want to run it off the cliff.

It takes a real cynic to believe that politicians purposefully want to ruin the economy.

For the country's sake and your own. Please vote Democrat.

CHARLES G. MCINTOSH

Gambrills

For my sake and everyone else's, I'm glad people voted Republican.

My car is in the shop because I ran it into the Busch/Cheney ditch: false (a runaway tire hit it on the beltway).

Republicans are the party of no: false.

Obama has a long term plan to balance the budget: comical. Also, it's easy to balance the budget if you raise taxes--that's the whole problem.

{kind=link}

*The recession was caused mostly by loose credit and a housing price bubble, particularly as a result of Fannie and Freddie. R's and D's I'm sure share the blame for lack of oversight, but it was Democrat Barney Frank who had the most power to affect the policies that led to the recession, but denied the existence of a problem even as the recession had started:

The Republicans have no credible plan to recover from recession. The Democrats are better able to balance the budget, witness President Clinton's large surplus and President George Bush's massive deficit at the end of their terms.

I don't know if Clinton had a surplus at the end of his term, and I'm not going to find out because I've already looked up a lot of shit for this post. So, if he did have a surplus, it's because of a positive business cycle, capital gains and income taxes from an asset bubble, and lack of a major war. Plus, using the deficits at the end of 2 particular Presidents' terms to prove that Democrats better balance the budget is the worst way to prove something since O.J. Simpson's glove.

Also, the credible way to recover from recession is to let producers keep more more of their own money so they can hire more people and invest in future production.

If the Republicans win the next election, they intend to go back to the disastrous policies of President Hoover that led to the great depression. Having run the economy into the ditch, they now want to run it off the cliff.

It takes a real cynic to believe that politicians purposefully want to ruin the economy.

For the country's sake and your own. Please vote Democrat.

CHARLES G. MCINTOSH

Gambrills

For my sake and everyone else's, I'm glad people voted Republican.

Friday, November 5, 2010

Harvard Academics Agree: Budget Balancing Is Best Done By Reducing Government Spending

The reason that many big government types love the economist John Meynard Keynes is that out of all of Keynes' ideas, they are able to single out his recommendation of government spending to stimulate the economy as support for what they want to do politically. The major argument against deficit spending (other than the fact that your kids eventually have to pay for the money you borrow) was that government spending 'crowds out' private investment. When the government prints money to spend on programs, the money supply is increased. When the supply of anything is increased, it's price goes down. So when the supply of money is increased, interest rates go down, and the private sector doesn't invest their money (in business improvements) because the return on investment isn't as good.

With the Federal Reserve announcing QE2, which is exactly what I just talked about in the last paragraph, The Economist picked a good time to talk about the issue. In Britain, they announced some "austerity measures", which is the proper British way to announce that a bunch of government jobs were being cut.

In America, reducing government is of course prohibited by the 88th amendment to the Constitution, so we tried to raise taxes. The money wasn't even used to balance the budget; it was used to pay for new tomfoolery and ballyhoo.

Now, normally this move could be supported by a cadre of Harvard economists. However, in this case, research by professors from Harvard and elsewhere conclude that the 'crowding out' theory holds water:

With the Federal Reserve announcing QE2, which is exactly what I just talked about in the last paragraph, The Economist picked a good time to talk about the issue. In Britain, they announced some "austerity measures", which is the proper British way to announce that a bunch of government jobs were being cut.

In America, reducing government is of course prohibited by the 88th amendment to the Constitution, so we tried to raise taxes. The money wasn't even used to balance the budget; it was used to pay for new tomfoolery and ballyhoo.

Now, normally this move could be supported by a cadre of Harvard economists. However, in this case, research by professors from Harvard and elsewhere conclude that the 'crowding out' theory holds water:

It found that a 1% rise in government consumption as a share of GDP eventually reduced private-sector consumption by 1.9%. Temporary spending to pick up economic slack may be useful but the long-term benefits of austerity seem clear.

Thursday, November 4, 2010

Recommended Reading

I'm not ashamed to admit that I don't read a whole lot--or at least it's not a prolific hobby of mine. TV is way better (admit it!); I work a lot; and if I start reading I quickly lose attention and/or want to go to sleep.

However, there are some things that I highly recommend. From the following list, you might notice that I "borrow" writing techniques, or outright plagiarize their work! Hey, they've figured out how to write well...I'm not here to reinvent the wheel.

So here they are, highly recommended:

1. The Economist. I've had a subscription for like 6 years and I love it. Don't worry, only like 10% of the magazine is about economics. Basically, they tell you just enough about a variety of topics that you know what other people are talking about, but not so much that you feel like you're doing homework or learning way too much about, say, the balance of trade deficit with our export partners. Plus I'm pretty sure it's published in England, and each time they replace a "z" with an "s", it makes you feel a little more cultured.

2. Shit My Dad Says. This is the funniest book I've ever read, and the greatest coffee table book ever. The writer tells stories about his dad, which are funny, primarily because there is a lot of cussing. The book was made into a CBS sitcom, which is not funny, primarily because there is no cussing.

3. La Liga Loca. This is a double whammy--a blog....about soccer. Having been to Barcelona once, I immediately declared myself "European" and developed a love for soccer. The writer of this blog shares the same snarkyness and cynicism that I pride myself on, and highlights how blogs can allow people who spend way to much of their life on their hobby to achieve a minimal amount of success. You too will soon learn that the La Liga's emphasis on finesse and flowing soccer is way better than the harsh hooliganism of the English Premier League and the fierce organization and largess of the German Bundesliga. (Note: it is appropriate to ignore the Italian Serie A due to corruption and a preponderance of thick black beards).

4. Stuff White People Like. Another coffee table book, the goal of this book is to provide you with the information you need to trick a white person into thinking you are their friend and therefore making them available to help you move. (Everyone knows how awful it is to pack your whole house up and schlep across town.) Such topics covered include "liking religions your parents don't belong to", "kitchen gadgets", and the "Toyota Prius". Particular care is given to avoid liking things that the "wrong kind of white people" like, such as Dane Cook.

However, there are some things that I highly recommend. From the following list, you might notice that I "borrow" writing techniques, or outright plagiarize their work! Hey, they've figured out how to write well...I'm not here to reinvent the wheel.

So here they are, highly recommended:

1. The Economist. I've had a subscription for like 6 years and I love it. Don't worry, only like 10% of the magazine is about economics. Basically, they tell you just enough about a variety of topics that you know what other people are talking about, but not so much that you feel like you're doing homework or learning way too much about, say, the balance of trade deficit with our export partners. Plus I'm pretty sure it's published in England, and each time they replace a "z" with an "s", it makes you feel a little more cultured.

2. Shit My Dad Says. This is the funniest book I've ever read, and the greatest coffee table book ever. The writer tells stories about his dad, which are funny, primarily because there is a lot of cussing. The book was made into a CBS sitcom, which is not funny, primarily because there is no cussing.

3. La Liga Loca. This is a double whammy--a blog....about soccer. Having been to Barcelona once, I immediately declared myself "European" and developed a love for soccer. The writer of this blog shares the same snarkyness and cynicism that I pride myself on, and highlights how blogs can allow people who spend way to much of their life on their hobby to achieve a minimal amount of success. You too will soon learn that the La Liga's emphasis on finesse and flowing soccer is way better than the harsh hooliganism of the English Premier League and the fierce organization and largess of the German Bundesliga. (Note: it is appropriate to ignore the Italian Serie A due to corruption and a preponderance of thick black beards).

{kind=link}

4. Stuff White People Like. Another coffee table book, the goal of this book is to provide you with the information you need to trick a white person into thinking you are their friend and therefore making them available to help you move. (Everyone knows how awful it is to pack your whole house up and schlep across town.) Such topics covered include "liking religions your parents don't belong to", "kitchen gadgets", and the "Toyota Prius". Particular care is given to avoid liking things that the "wrong kind of white people" like, such as Dane Cook.

Return To Glory

Hey party people! It's been a long time. We're getting the band blog back together! Now that the business of getting actual politicians elected has been accomplished, it's time to re-focus on what the world has been clamoring for: wandering and purposeless rants conducted safely from my living room couch. If you feel that not enough people express their opinions on topics that you don't really care about, then this blog is for you!

Here are the rules, some of which are new.

1. The content can be about anything, not just politics. The only requisite is that it interests me, and hopefully you too will find either the content or the entertainment value worthwhile.

2. No advertisements. Nothing against blogs that try and monetize, but that's not my deal.

3. Rumors are allowed. Here's why:

I found myself involved in an internal debate regarding the professionalism of publishing a rumor, and after nearly 6 minutes of deliberation, I have determined that publishing rumors is acceptable for the following reasons:

-I will never publish anything that I know to be false.

- I offer a disclaimer and do not claim such rumors to be facts.

- Publishing a rumor offers the readership of this blog a chance to research the rumor to see if it's true, and if it is true, we have contributed to the body of knowledge. In other words, if I publish a rumor about something crazy going on, then like 8 people keep their eyes peeled for crazy goings on, we are more likely to find out the craziness if it is really happening.

-'Professionalism' implies a profession--i.e. a money making exercise--and seeing that this blog is a consuming asset rather than a producing asset--i.e. I don't get a red cent for doing this--I can be as professional or unprofessional as I want.

Here are the rules, some of which are new.

1. The content can be about anything, not just politics. The only requisite is that it interests me, and hopefully you too will find either the content or the entertainment value worthwhile.

2. No advertisements. Nothing against blogs that try and monetize, but that's not my deal.

3. Rumors are allowed. Here's why:

I found myself involved in an internal debate regarding the professionalism of publishing a rumor, and after nearly 6 minutes of deliberation, I have determined that publishing rumors is acceptable for the following reasons:

-I will never publish anything that I know to be false.

- I offer a disclaimer and do not claim such rumors to be facts.

- Publishing a rumor offers the readership of this blog a chance to research the rumor to see if it's true, and if it is true, we have contributed to the body of knowledge. In other words, if I publish a rumor about something crazy going on, then like 8 people keep their eyes peeled for crazy goings on, we are more likely to find out the craziness if it is really happening.

-'Professionalism' implies a profession--i.e. a money making exercise--and seeing that this blog is a consuming asset rather than a producing asset--i.e. I don't get a red cent for doing this--I can be as professional or unprofessional as I want.

4. I get super annoyed by the spam, but blogger claims to be able to automatically detect spam so I'm going to leave the comments unmoderated for now and see what happens. If you leave a comment it will most likely be posted. I can only remember deleting 1 comment and it was when the daughter of an elected official was called an awful name by the commenter. It doesn't matter to me if you are anonymous or use a fake name, but your right to free speech will be balanced by my prerogative to deny useless or inappropriate comments.

That's about it. Happy Reading!

Subscribe to:

Posts (Atom)